1 Industry Snapshot

1.1 Local Finance

Key Points:

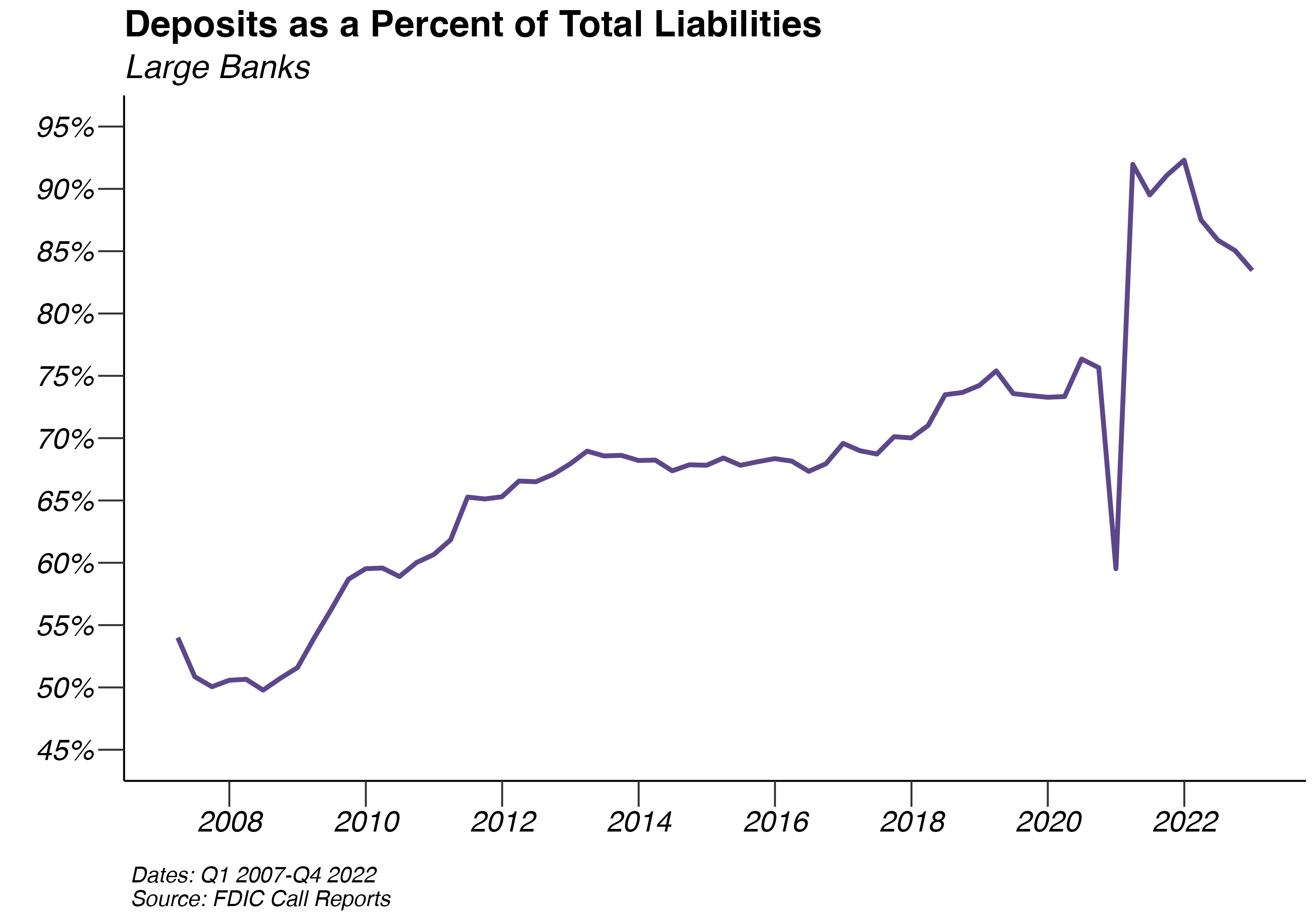

- Large banks experienced a decrease in deposits as a percentage of liabilities with 83.46% as of 12/31/2022 compared with 92.3% the year prior.

- As of 12/31/2022, small banks’ net income is -12.51% lower than the same time last year.

- Both small and large banks exceeded their pre-recession levels for return on assets.

FDIC Call Reports are released for all banks in the U.S., providing financial statement information to the public that is otherwise unavailable for private companies. The Local Finance section reports and analyzes banks that have a presence in Santa Barbara County. Using the data from FDIC Summary of Deposits, we examine each bank’s activity and health on a local level. For banks with an international presence, we are not able to factor out their international operations due to limitations in the data provided by the FDIC Call Reports. Therefore, 6 out of the 19 institutions have an aggregated total of both domestic and foreign operations for their assets and liabilities. The difference makes up about 4% of the total – which does not materially change the analysis on a local level.

In this section, we have two categories: large banks and small banks. Large banks are banks that operate on both regional and national levels; whereas, small banks are comprised of solely regional banks and banks with less than $2 billion in total assets. Big banks in this year’s data include Rabobank, Union Bank, Wells Fargo, JP Morgan Chase, Bank of America, First Republic Bank, Bank of the West, The Northern Trust Company, Pacific Western Bank, U.S. Bank, Citizens Business Bank, First Bank, and Banc of California. For our analysis on small banks, we have included American Riviera Bank, Community West Bank, Pacific Premier Bank, Montecito Bank & Trust, Community Bank of Santa Maria, Bank of the Sierra, and Farmers and Merchants Bank of Long Beach.

The data in this section has been adjusted for inflation; therefore, all numbers in the section are in terms of 2009 dollars. Nominal numbers have been adjusted to real numbers on a quarterly basis with the CPI from the Federal Reserve Economic Data, giving us a more comporable analysis of banking trends, particularly in times of large price movements. Moreover, all metrics describe totals for the industry unless otherwise specified.

1.1.1 Savings and Time Deposits

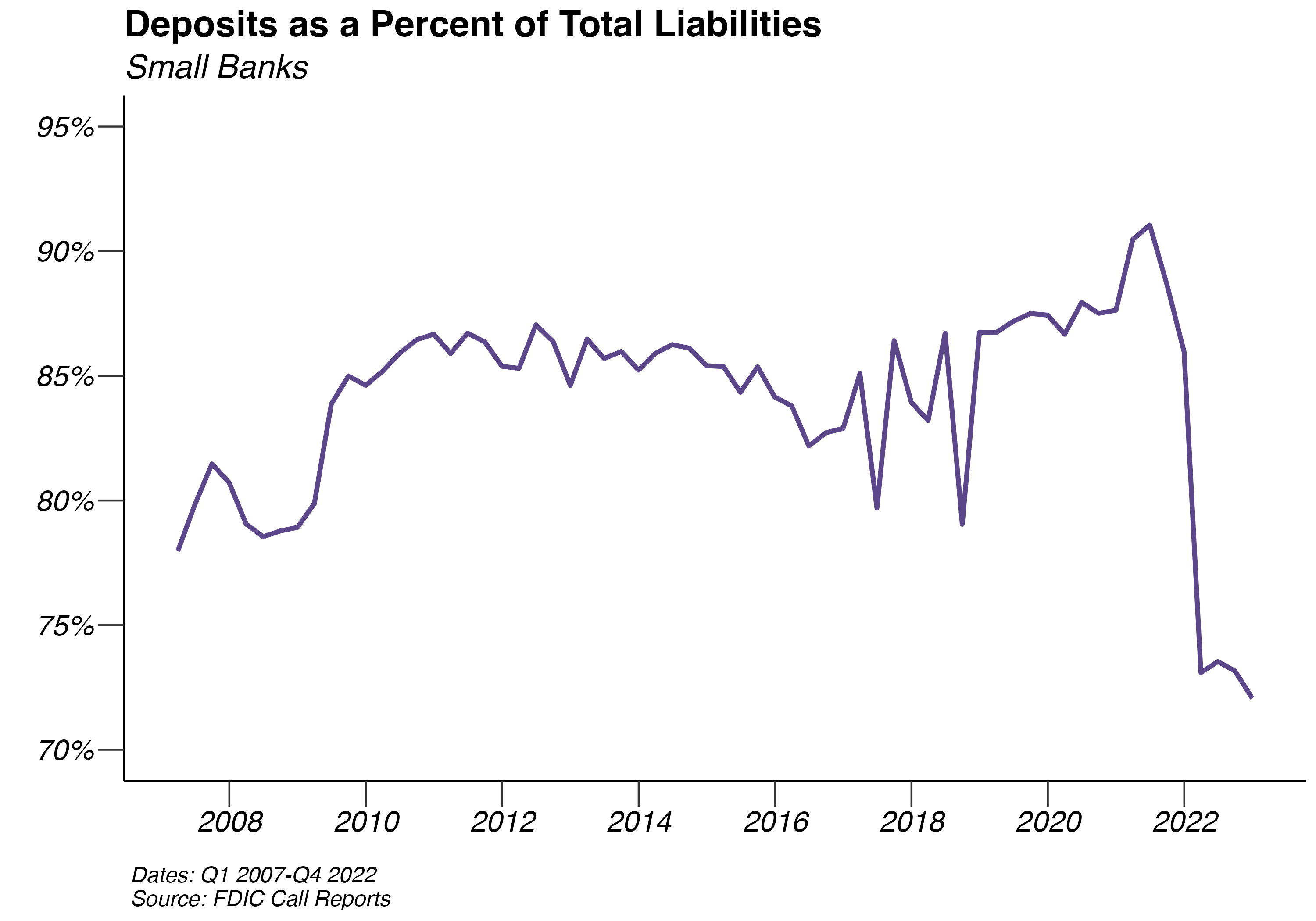

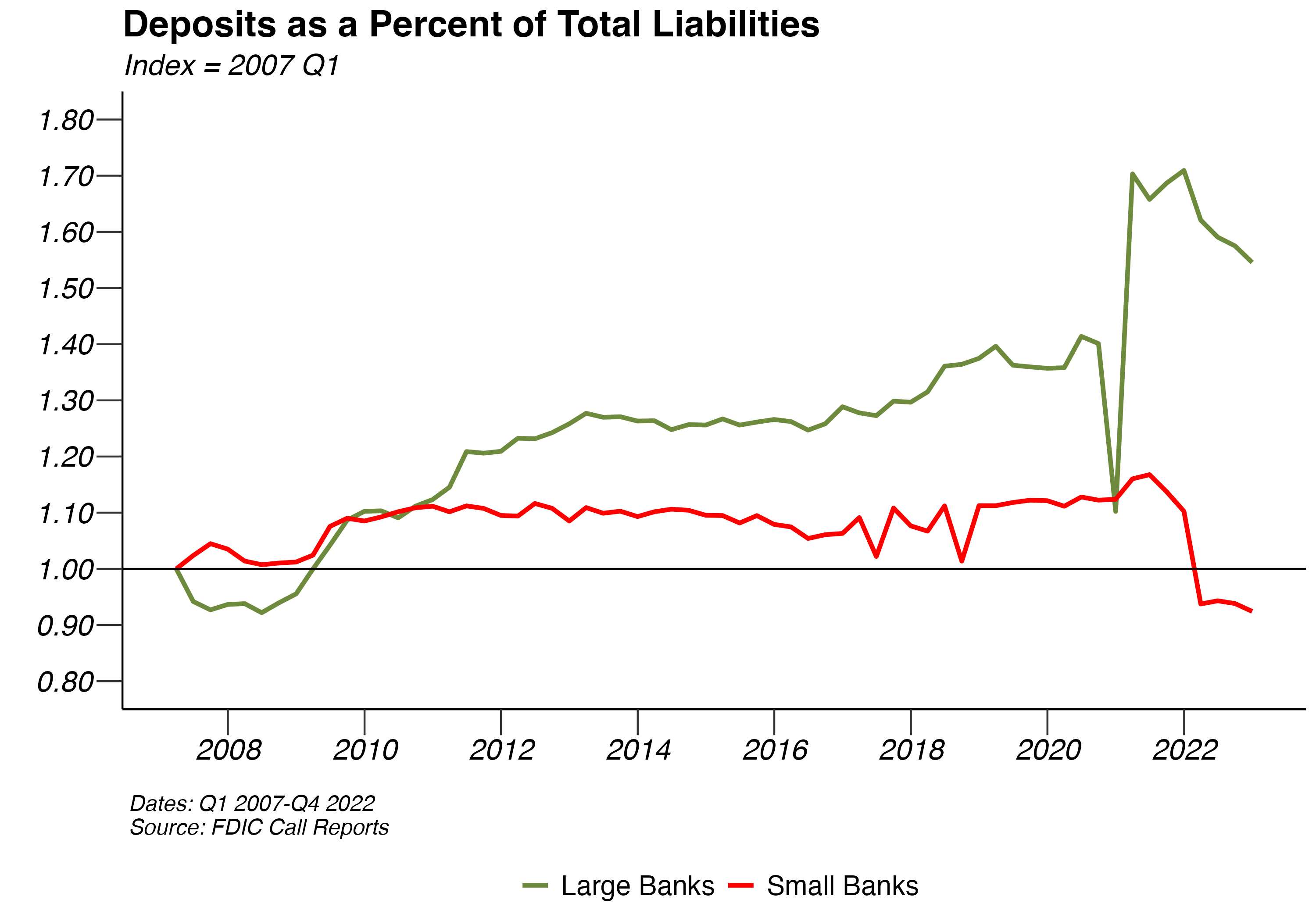

Deposits held by banks represent the vast majority of liabilities for both categories. As of 12/31/2022, large regional banks held 83.46% of their total liabilities as deposits, a decrease from 92.3% the same time last year. On the other hand, small regional banks held 72.07% of their total liabilities as domestic deposits, down -13.89 percentage points from last year. Since deposits represent such a large percentage of total liabilities, it is important to understand the trends within each bank category in order to understand where consumers are depositing money.

Small and large banks display similar trends in terms of deposits as a percentage of total liabilities. Until this year, large banks had been steadily increasing their deposits as a percent of total liabilities over the past few years, whereas small banks have been more volatile.

Since the Great Recession, both small and large banks have increased their percent of deposits as a fraction of liabilities. This trend peaked for small regional banks at 91.05% on 06/30/2021, 10.34 percentage points higher than at the end of 2007. Deposits as a fraction of liabilities for large banks peaked at 92.3% on 12/31/2021, 41.73 percentage points higher than it was at the end of 2007.

In 2022, the banking industry in Santa Barbara County consisted of 20 institutions with $17,952,514,000 in deposits. Compared with the previous year, there was a decrease of -14.47% in deposits with an increase in the number of banks. The numbers in the table below are in nominal terms since the change in CPI from 2021 to 2022 was small, making the deposits relatively comparable. First Bank experienced the largest increase in deposits with a change of 18.49%. Bank of The Sierra had the largest decline in deposits, falling from $48,467,000 to $63,226,000 or -23.34%. As banks know when their deposits will be measured every year, we cannot rule out some level of manipulation of deposits that leads to large fluctuations.

|

Position

|

Name

|

Position Change

|

Deposit (in thousands)

|

Market Share

|

||

|---|---|---|---|---|---|---|

|

2022

|

2021

|

Change

|

2022

|

|||

| 1 | Wells Fargo | $3,058,799 | $3,048,912 | -0.32% | 17.04% | |

| 2 | Bank of America | $2,560,865 | $2,465,031 | -3.74% | 14.26% | |

| 3 | JPMorgan Chase Bank | +1 | $2,404,277 | $2,317,967 | -3.59% | 13.39% |

| 4 | Mufg Union Bank | NA | $2,366,579 | $2,126,181 | -10.16% | 13.18% |

| 5 | Montecito Bank & Trust | $1,970,211 | $1,715,921 | -12.91% | 10.97% | |

| 6 | Mechanics Bank | $1,263,690 | $1,246,275 | -1.38% | 7.04% | |

| 7 | American Riviera Bank | $871,855 | $759,516 | -12.89% | 4.86% | |

| 8 | Pacific Premier Bank | $685,184 | $663,661 | -3.14% | 3.82% | |

| 9 | First Republic Bank | +1 | $669,765 | $568,485 | -15.12% | 3.73% |

| 10 | Community West Bank | -1 | $582,499 | $536,986 | -7.81% | 3.24% |

| 11 | Community Bank of Santa Maria | $389,162 | $339,464 | -12.77% | 2.17% | |

| 12 | Bank of the West | $238,084 | $260,552 | 9.44% | 1.33% | |

| 13 | Pacific Western Bank | +1 | $234,692 | $237,808 | 1.33% | 1.31% |

| 14 | First Bank | +1 | $193,217 | $228,952 | 18.49% | 1.08% |

| 15 | The Northern Trust Company | -2 | $189,360 | $179,156 | -5.39% | 1.05% |

| 16 | Farmers and Merchants Bank of Long Beach | +2 | $71,073 | $64,206 | -9.66% | 0.40% |

| 17 | U.S. Bank | -1 | $67,524 | $59,949 | -11.22% | 0.38% |

| 18 | Bank of The Sierra | -1 | $63,226 | $48,467 | -23.34% | 0.35% |

| 19 | Banc of California | $50,684 | $47,199 | -6.88% | 0.28% | |

| 20 | Citizens Business Bank | $21,768 | $21,106 | -3.04% | 0.12% | |

| Totals | $17,952,514 | $15,355,639 | -14.47% | 100.0% | ||

1.1.2 The Herfindahl-Hirschman Index

The Herfindahl-Hirschman Index (HHI) is a commonly used measure of industry concentration. Ranging from 0 to 1, the HHI is found by summing the squared market shares of all the firms. When the HHI is 0, a market has a large number of equally sized firms; on the other hand, when the HHI is 1, a market has only one firm. According to the Department of Justice, any market with a HHI between 0.15 and 0.25 is considered to be moderately concentrated. When a market exceeds 0.25, the Department of Justice finds it to be a concentrated market, which may require further review before any mergers can occur.

For Santa Barbara County, the current HHI is 0.109. Therefore, the current banking industry in Santa Barbara is un-concentrated. The HHI for the County decreased by 1.44% compared with last year’s HHI of 0.1106.

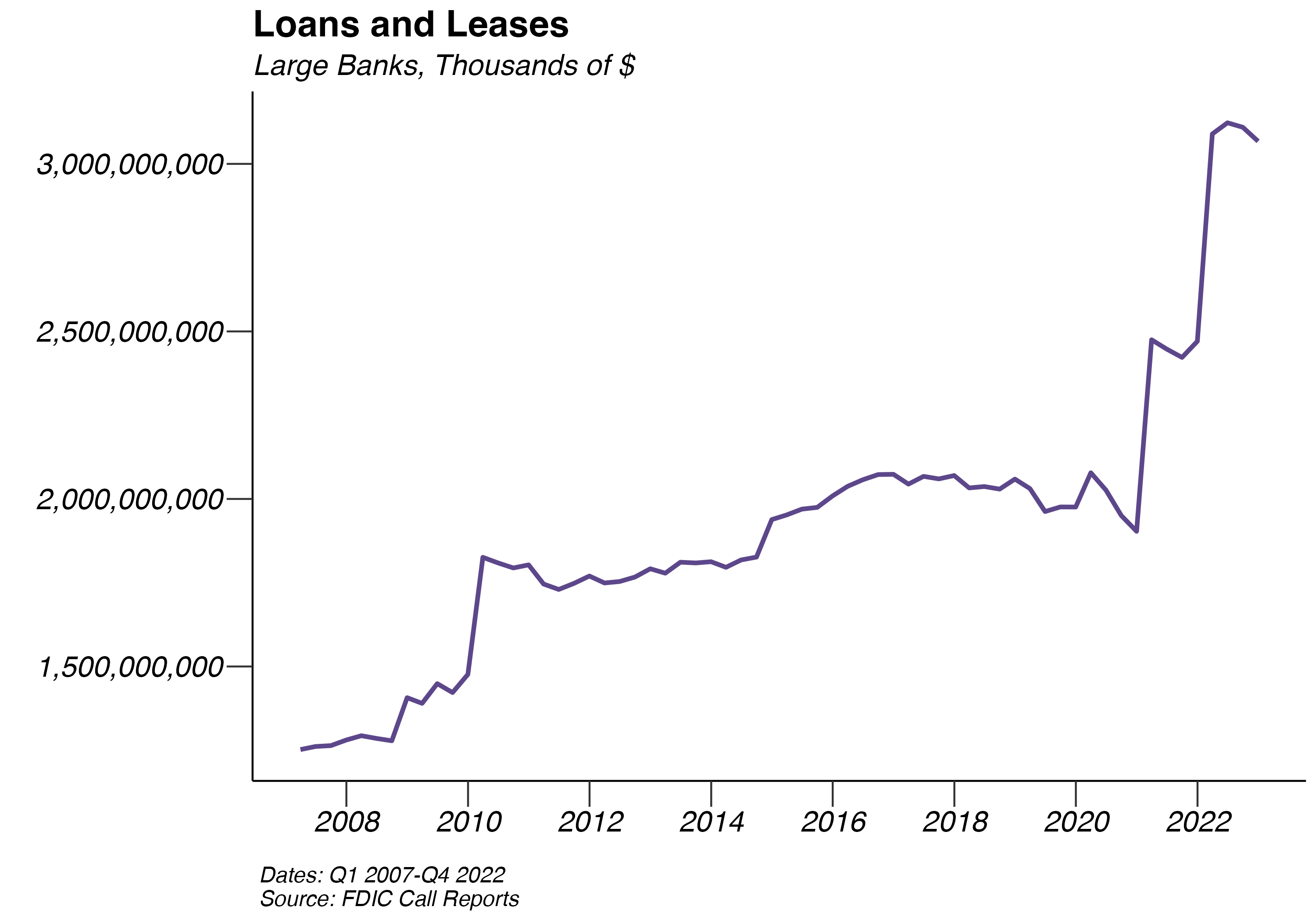

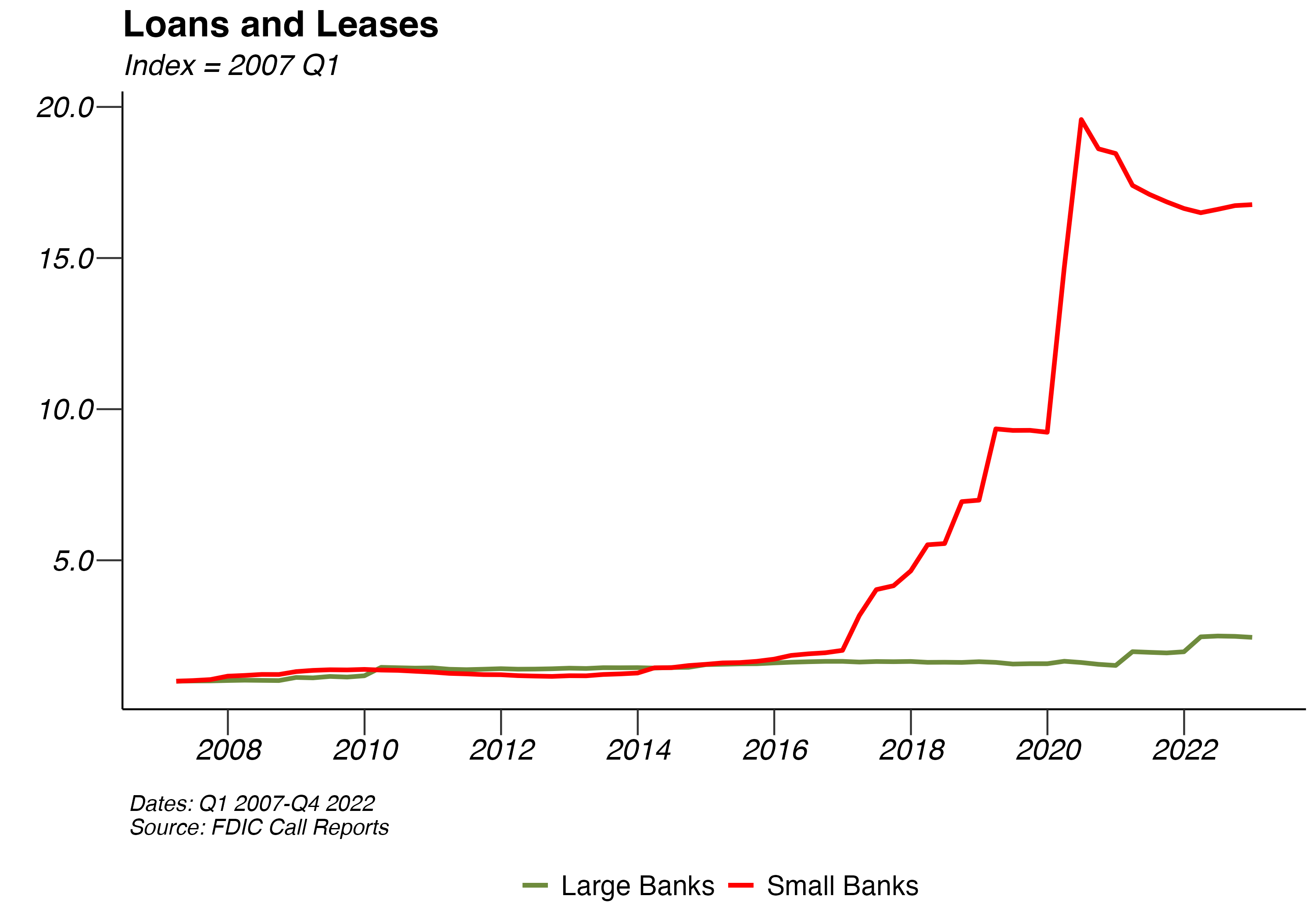

1.1.3 Loans and Leases

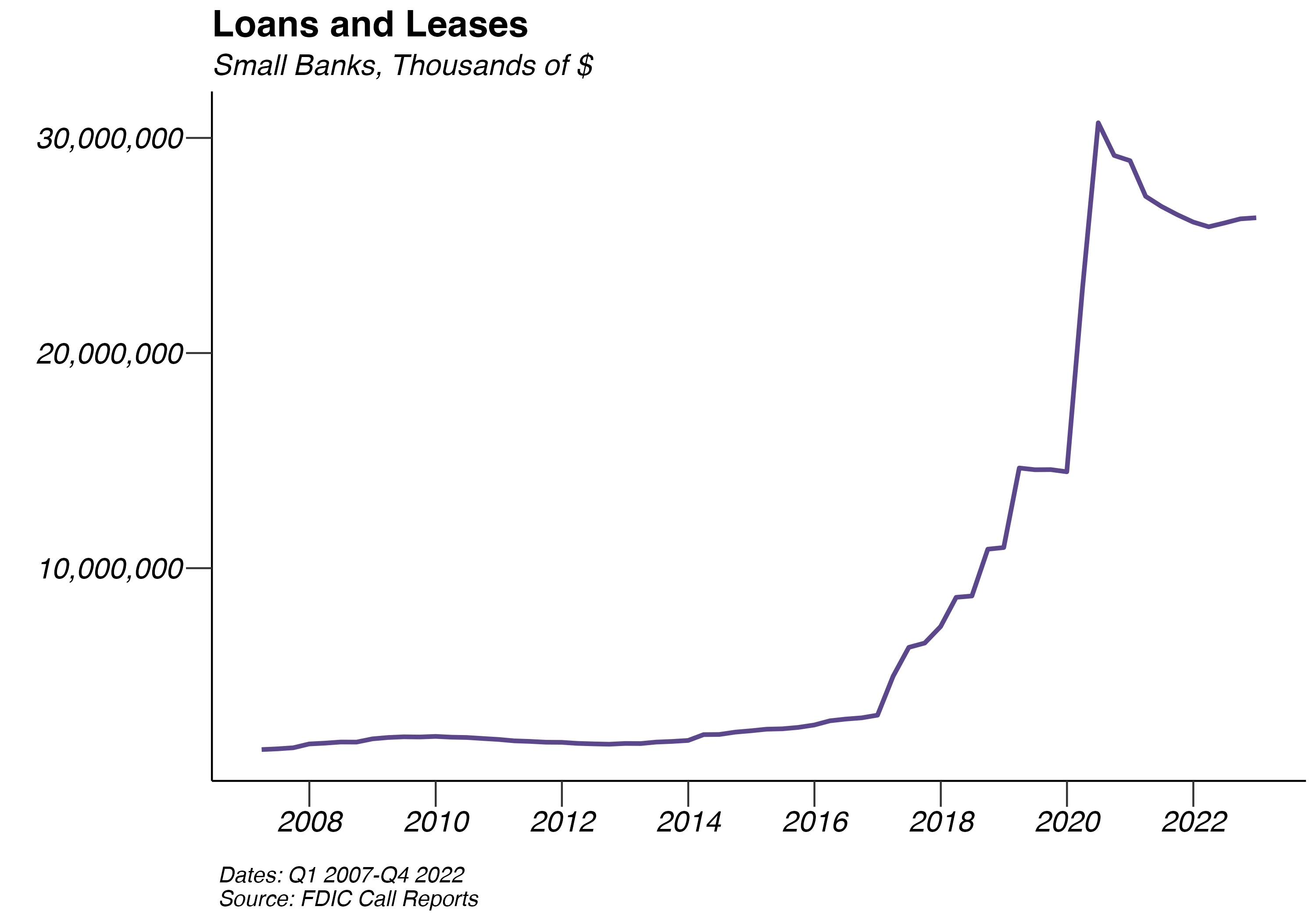

In the past year, loans and leases appear to be trending upwards for large banks, while small banks experience a slow decline following the first quarter of 2019. The average quarterly growth rate for large banks between 12/31/2021 and 12/31/2022 was 5.56%, a decrease from that of 6.74% during the year prior. Since the first quarter of 2007, the average quarterly growth rate of loans and leases for large banks has been 1.43%.

Between 12/31/2021 and 12/31/2022, small banks saw an average quarterly rise in loans and leases of 0.19%, lower than their average growth rate over the previous year, which was -2.56%. In total, loans and leases for these banks rose from $26,089,619 to $26,289,241. The average quarterly growth rate of loans and leases since the first quarter of 2007 is 4.58%.

Both small and large banks saw sharp increases in loans throughout 2020, with the COVID-19 pandemic and subsequent quantitative easing policies. Loans have seen some dropoff starting in 2021 for both large and small banks.

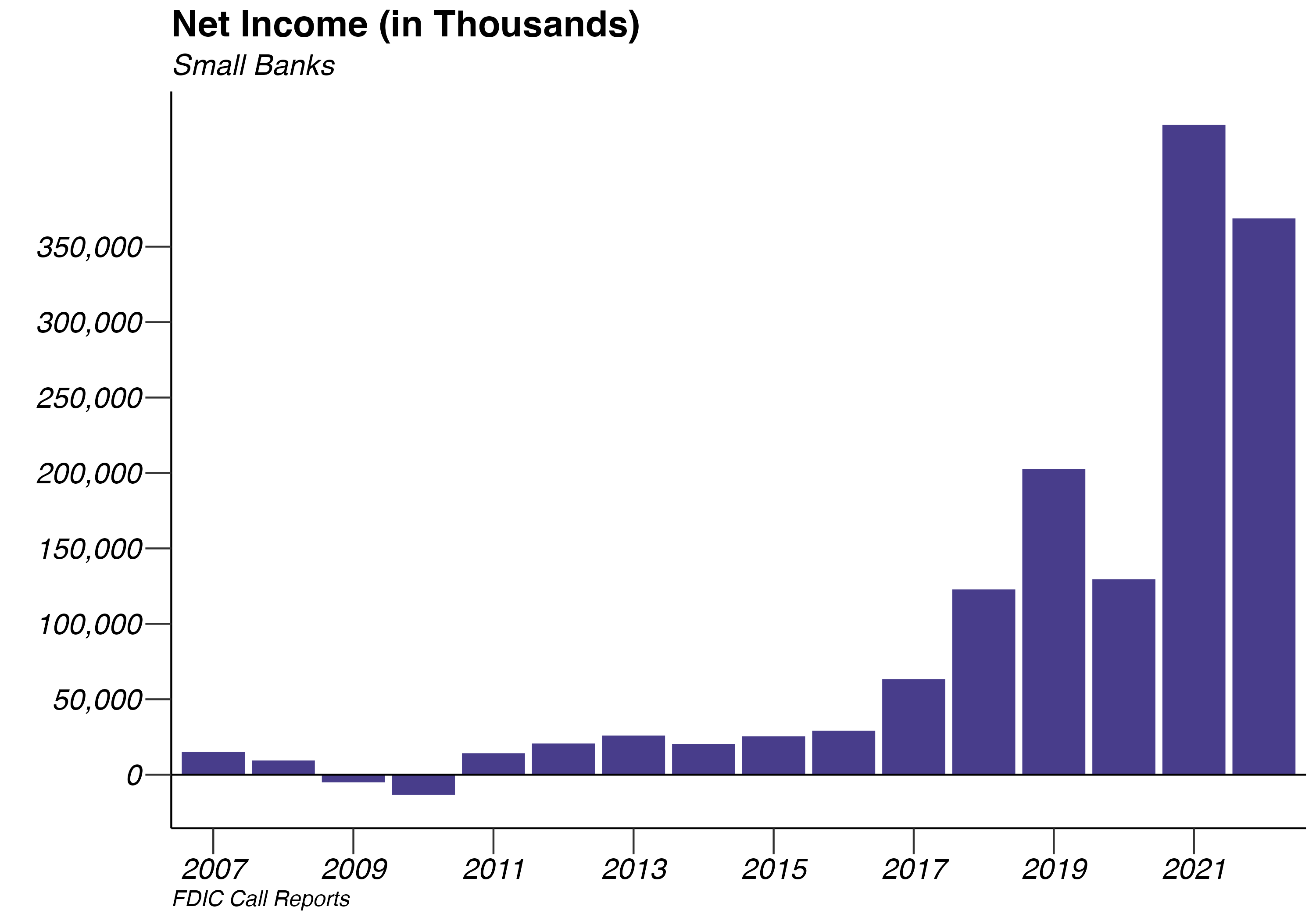

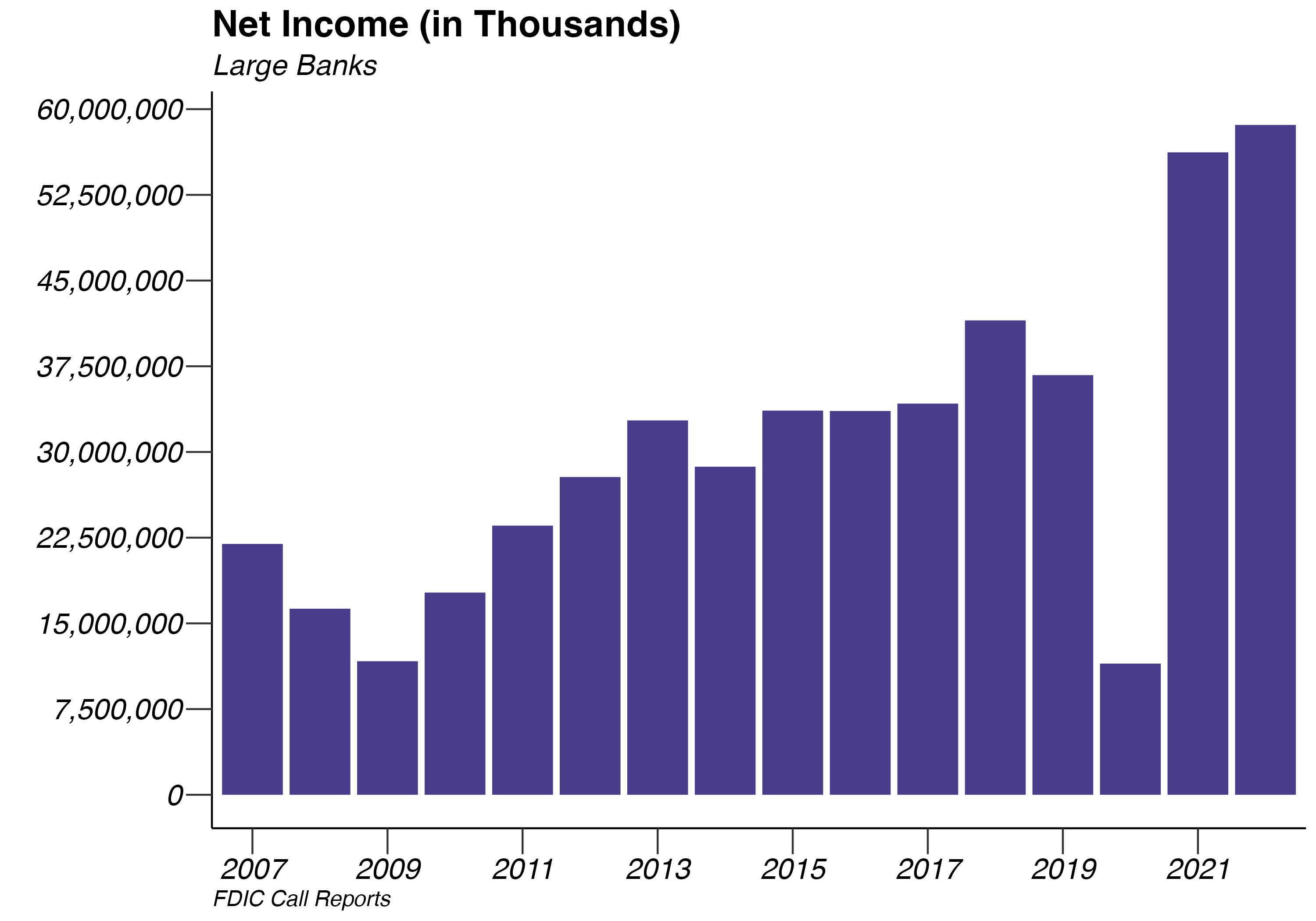

1.1.4 Net Income

Real net income decreased by -12.51% for small banks between 2021 and 2022, falling from $282,402 to $247,080. Small banks’ net income has recovered tremendously after seeing losses in 2009 and 2010. For large banks, net income decreased by -5.1%, reversing the upward trend of the past few years.

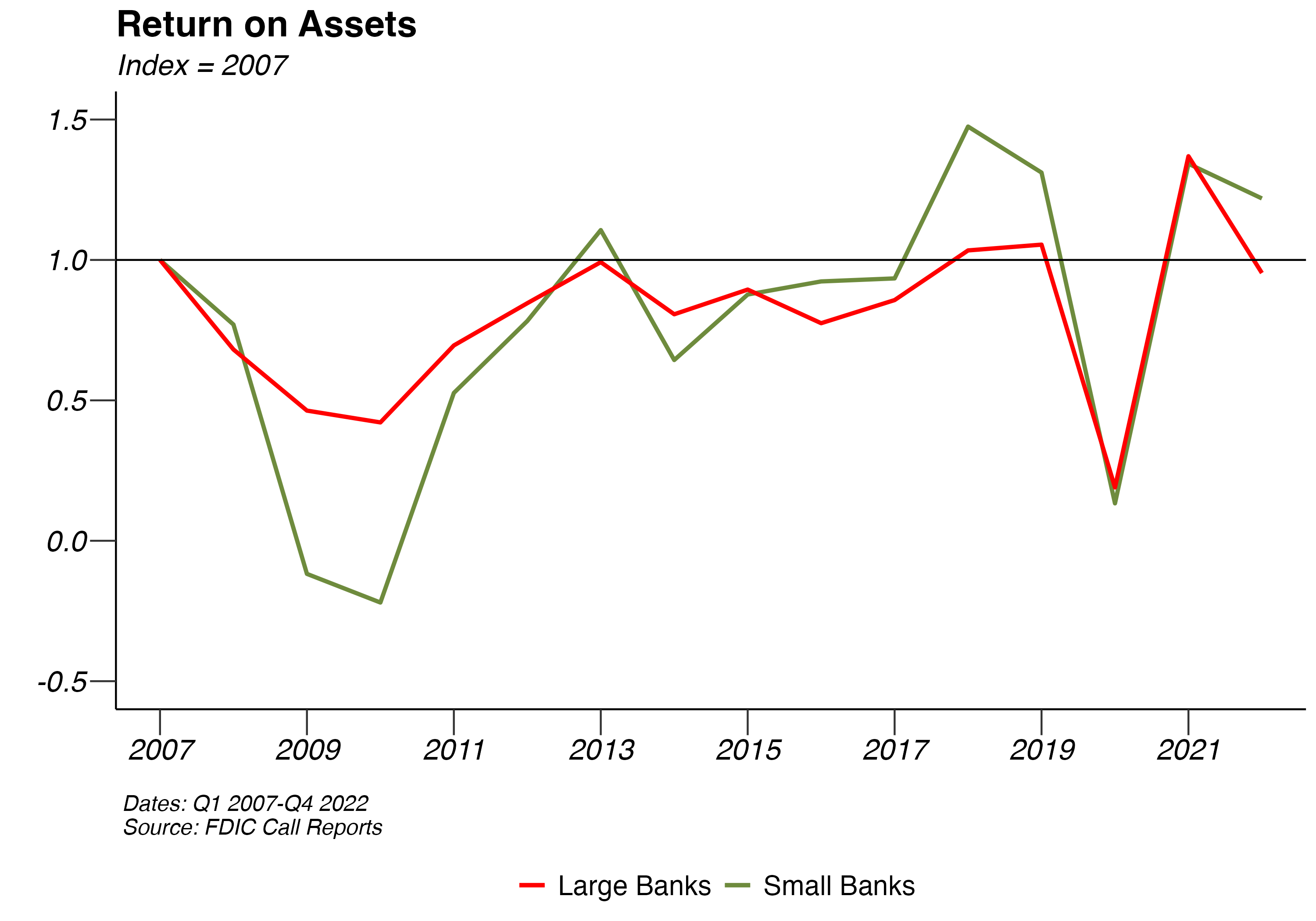

Since the collapse of the financial markets in 2008, banks have experienced a healthy rebound. Although, simply looking at the value of net income does not account for the increase in the size of many banks. In order to take this into account, we divide total net income for the industry in a given year by the industry’s year end total assets to calculate the industry’s Return on Assets (ROA). The ROA graph demonstrates the industry’s return on assets this year compared with that in 2007. Both small and large banks have surpassed their pre-recession levels in 2019. In 2014, the total return on assets for both large and small banks declined, but there appears to be a robust rebound. As of the end of 2022, large banks stand 4.65% lower than 2007 return on assets while small banks are now 21.9% higher than 2007 levels.

1.1.5 Pension

The Center for Retirement Research at Boston College collects public plan-level data for 220 states and local pension plans since 2001. Among these plans, we focus specifically on four pension systems: California PERF, University of California Retirement Plan, California State Teachers’ Retirement System, and Colorado Public Employee Retirement Association-School Division. When it comes to evaluating the performance of investments, there are a few key measures that investors can consider.

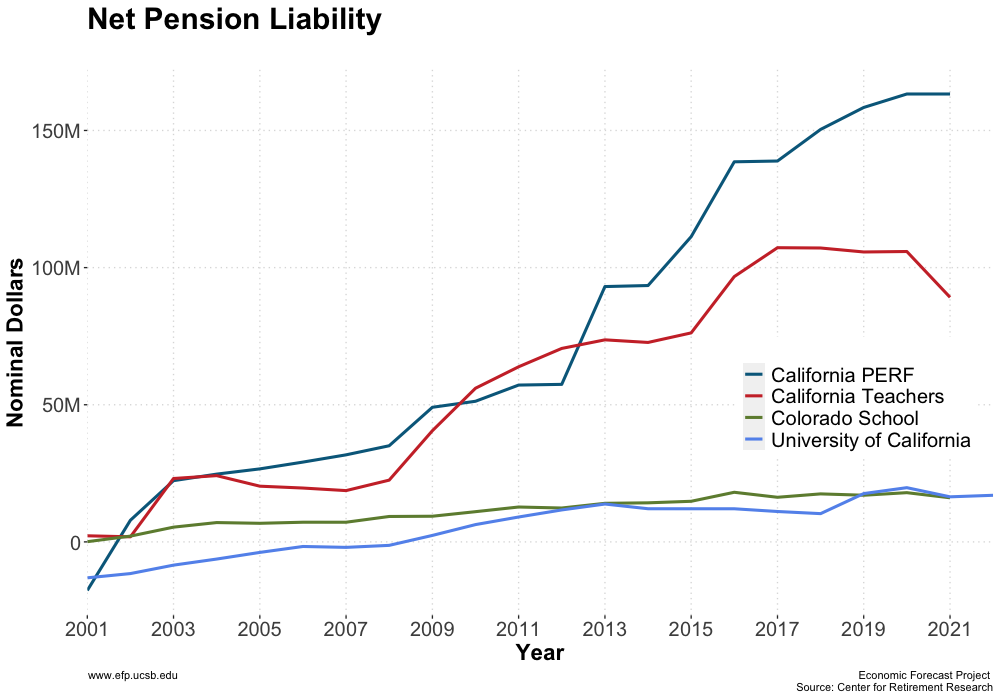

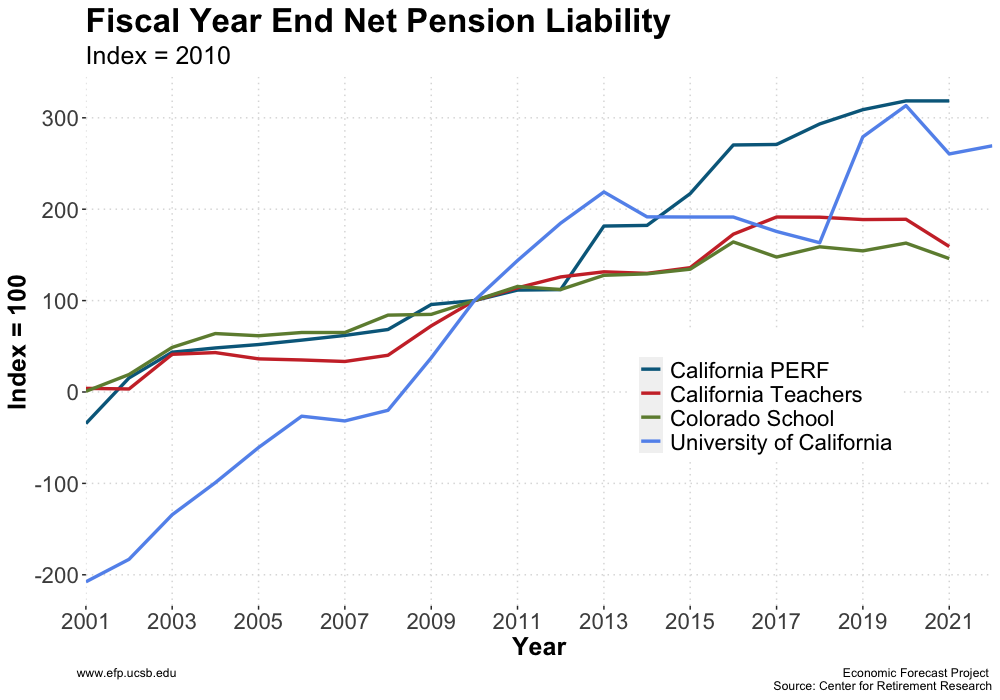

The net pension liability (NPL) is a measure of the difference between the present value of pension benefits earned by employees and the assets available to pay for those benefits. All four pension groups have seen a steady increase in their net pension liability over the years, indicating potential funding challenges in meeting their pension obligations. Since the base year of 2010, the NPL for California PERF, University of California, California Teachers, and Colorado School has increased by 218.49%, 160.45%, 59.18%, and 45.98% respectively, as of 2021. The rise in NPL for California PERF is particularly notable, which can be attributed to a combination of factors, including longer life expectancies, lower investment returns, and changes to actuarial assumptions.

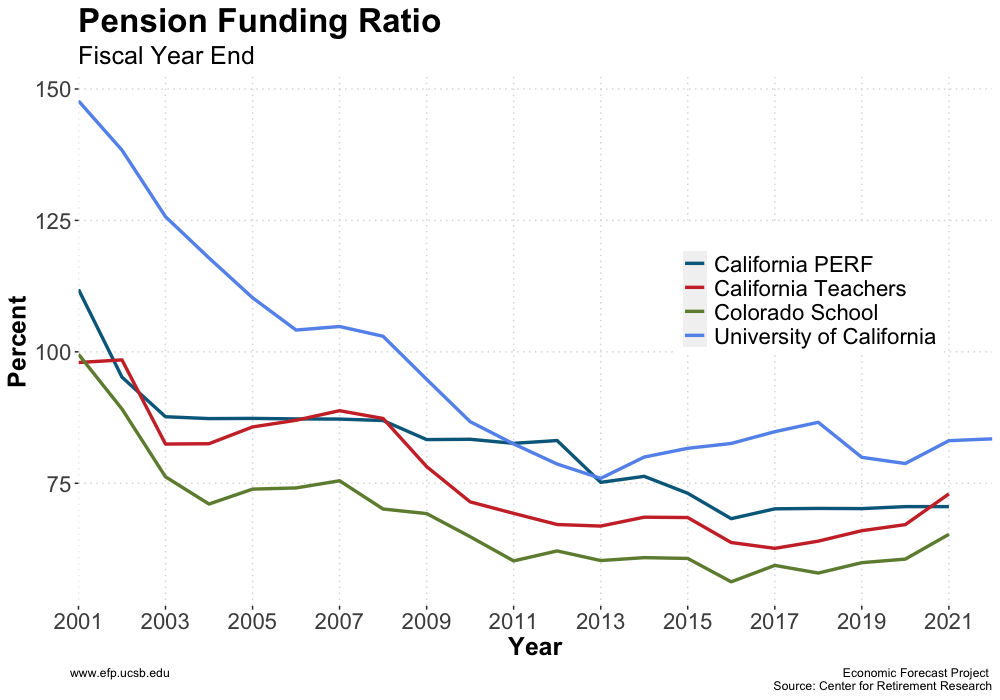

While NPL helps to assess the financial risk associated with a pension plan, the pension funding ratio can serve as a crucial metric for evaluating the financial soundness of a pension plan by assessing the correlation between its assets and liabilities. It is expressed as a percentage and is calculated by dividing the value of the plan’s assets by the value of its liabilities. A funding ratio of 100% or greater indicates that a plan has enough assets to cover its liabilities, while a ratio below 100% indicates a shortfall. The four pension plans all have become increasingly underfunded over the years, which is a cause for concern for their ability to provide retirement benefits to current and future retirees. Among all four plans, the University of California plan has consistently held the highest funding ratio among all four plans, albeit experiencing considerable declines from 147.73% in 2001 to 83.45% in 2022, which points to a substantial underfunding concern.

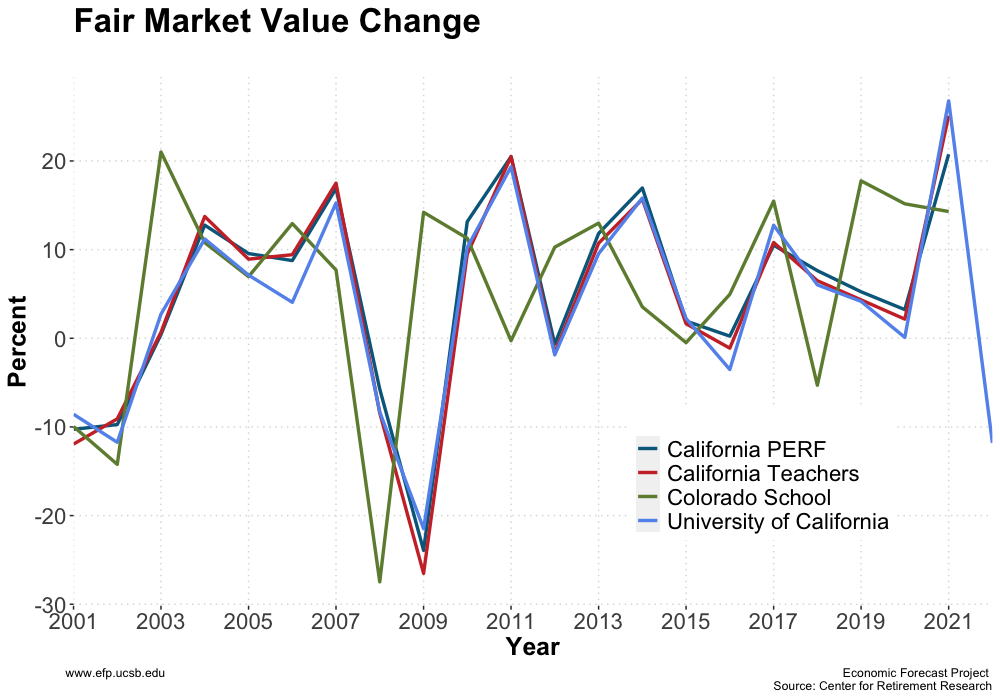

Percent fair value change is a measure that tells us how much the fair value of an asset or liability has changed over a specific period of time, expressed as a percentage of its original value. The percent fair value change of each fund varies widely from year to year. All four pension plans had experienced significant losses in 2008 and 2009 due to the financial crisis. However, they were all able to bounce back to the original level within one to two years. As of 2021, the fair market value change for each pension plan is 20.75%, 26.77%, 25.11%, and 14.3% respectively. These numbers highlight the varying levels of success that each pension plan has had in maintaining or increasing their fair market value. It’s worth noting that there are a variety of factors that can influence the fair value change of an asset or liability, including market conditions, economic factors, and geopolitical events.

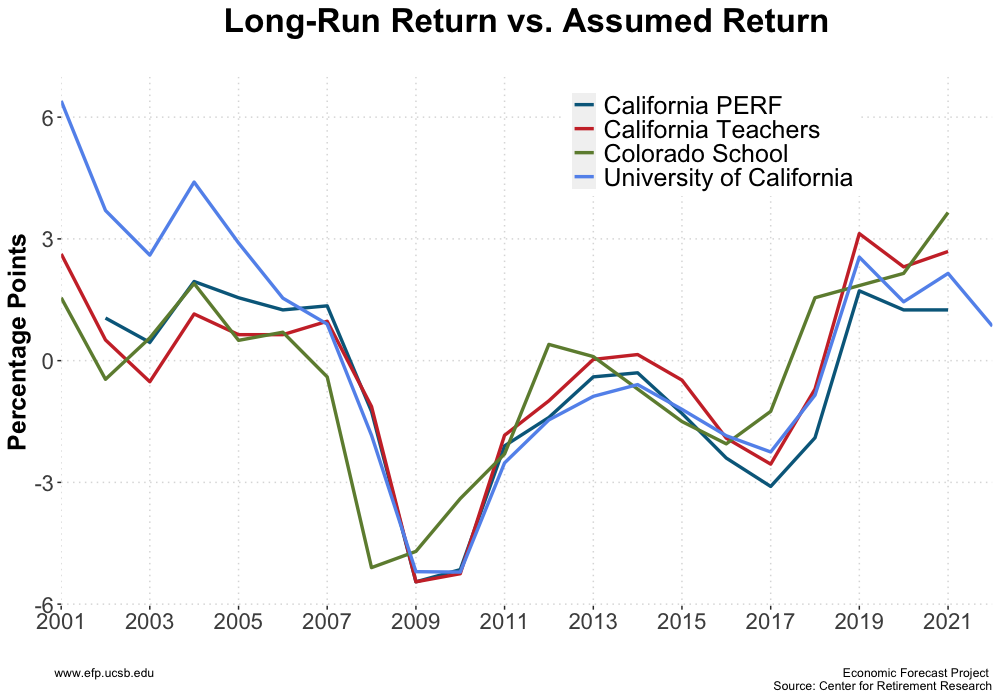

In addition, comparing the long run return to the assumed return can help investors evaluate the performance of their investments. If an investment consistently achieves a return that is lower than the assumed return, investors may want to consider reallocating their investments to other assets or strategies. In 2001, the University of California plan had the highest positive return of 6.04% compared to the assumed return. Since then, the four pension plans tend to rise and decline together, exhibiting a similar trend pattern across time periods. In 2021, the difference between long-run and assumed return for each pension plan is 1.25%, 2.15%, 2.69%, and 3.65% respectively.

From the perspective of state and local governments, one of the key challenges to balancing budgets is the need to fund pension systems. Three of the largest pension funds that affect our local community are calPERS, calTeachers, and UCRP. The reported total pension liabilities of each pension fund is $329 billion, $139 billion, and $88 billion respectively. Each of these funds reports an unfunded ratio, i.e. fraction of liabilities for which there are insufficient fund assets, of 27.44%, 28.39%, and 20.5%, respectively.

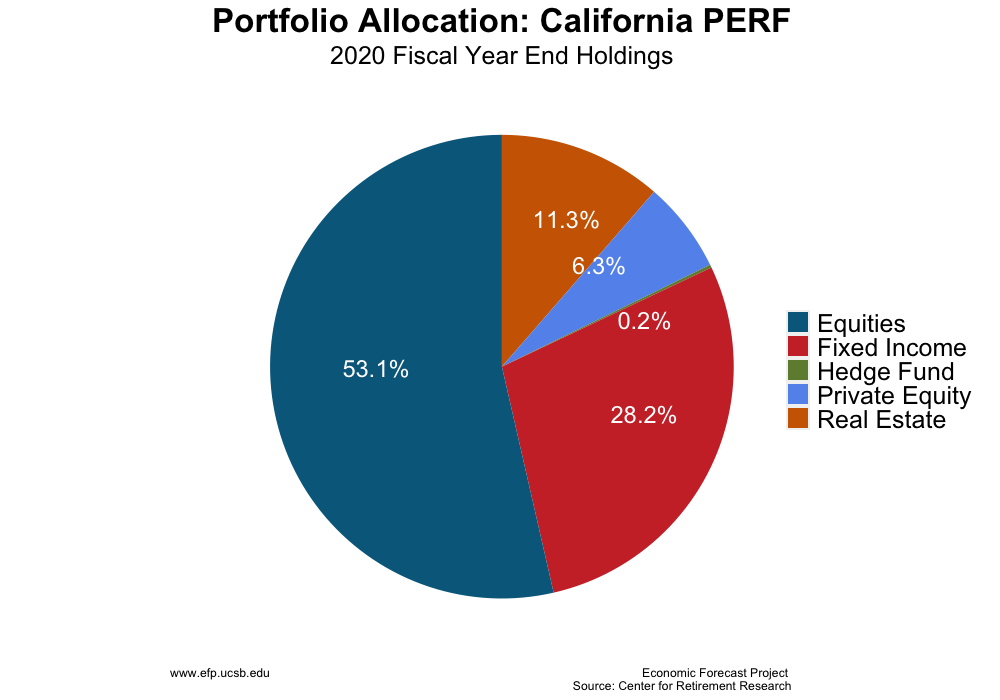

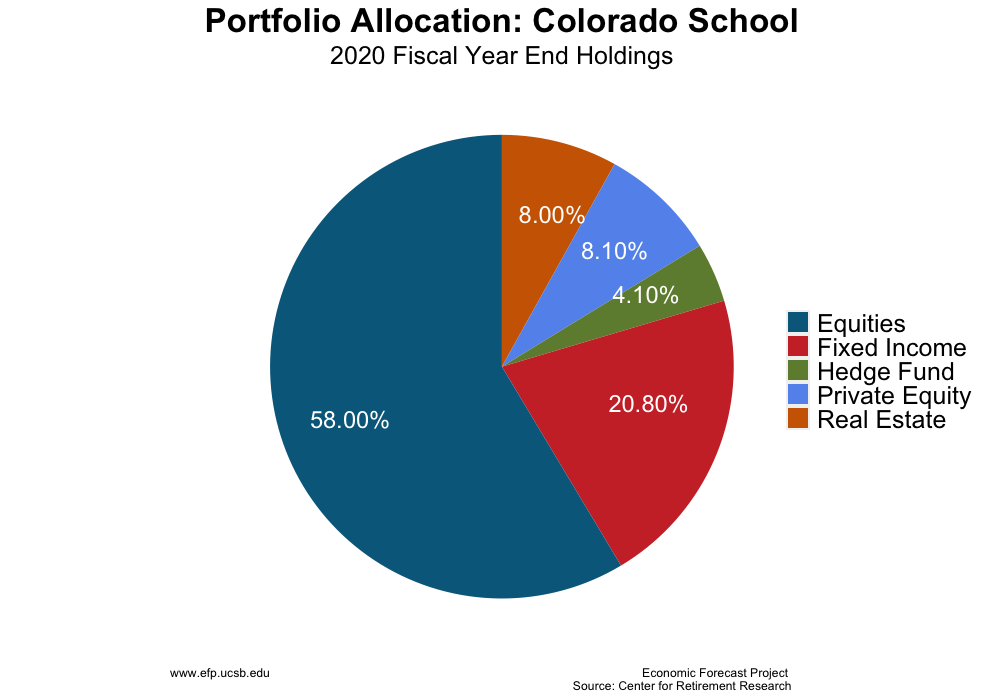

The liabilities data reported by pension funds while informative are misleading. In particular, annual financial reports produced by pension funds follow what are known as the GASB 67 guidelines. A crucial assumption necessary to calculate total pension liabilities is the assumed return of fund assets. The reported data all assume an annual rate of return above 7%. The key flaw in these assumptions is that funds are allowed to implicitly assume that the assets and liabilities of the fund are equally as risky. This is not necessarily the case. The graphs below show the portfolio allocation of each pension fund. The asset mix of all these pension funds is heavily tilted toward equities, which tend to be higher risk assets, as opposed to fixed income. Pension liabilities, on the other hand, are much more certain, i.e. less risky, than suggested by the asset mix of these funds.

To provide both a more conservative picture of the health of pension funds and one that treats pension liabilities as more certain (less risky), pension fund liabilities should be computed using, for example, risk free rates of return. One commonly used measure of the risk free rate of return is the return on 10 year treasury bonds. The graph below shows the position of these three pension funds using a risk free rate of 2.0%. The difference between the data reported and that implied by a risk free rate is quite stark. The total liabilities and unfunded ratio of each fund roughly doubles. While both the reported data and adjusted data presented below highlight the difficulty of funding these pension systems, the adjusted data shows that substantially more work must be done to balance budgets than may be recognized by local governments.

1.2 Oil and Gas

Key Points:

- California’s production of crude oil has been declining since the late 1980s and decreased by 3.38% between 2021 and 2022.

- Crude oil prices increased by -23.55% from July 2021 to July 2022.

California’s field production of crude oil has been decreasing every year since 2014. Oil production decreased in 2022 by 3.38% compared to the decrease in oil production in 2021 of 0.62%. In 2020, oil production decreased by 1%. From 2018 to 2019, oil production decreased by 1%.

In addition, oil prices have been increasing sharply from their lowest-ever price of in April 2020. Oil prices fell by -23.55% from July 2021 to July 2022. So far in 2022, the price for WTI-Texas has averaged $79, compared with an average of $93.59 in 2021. From July 2020 to 2021, oil prices increased by 68%. Of particular note during 2022 is the sharp increase in oil prices resulting from the invasion of Ukraine. However, price growth has started to slow down, with the average price of oil declining from June to July of 2022.

1.2.1 Federal Offshore Oil Production

Federal offshore oil production has been declining since the mid-1990s and has now reached the lowest level in the recorded data. So far in 2022, federal offshore oil production has averaged 211 thousand barrels per month, a -37.08% decrease compared with the average of 335.33 thousand barrels per month in 2021. At its peak in 1995, federal offshore oil production reached 6,312 barrels per month.

1.3 Agriculture

Key Points

- Total crop value increased by 5.44%, from $1.82 billion in 2020 to $1.92 billion in 2021.

- The total value of strawberries, the county’s highest-grossing crop, increased by 16.81% from $727.4 million in 2020 to $849.7 million in 2021.

- Total sales of wine grapes reached 105.15 in 2021, a increase of 12% compared with 2020.

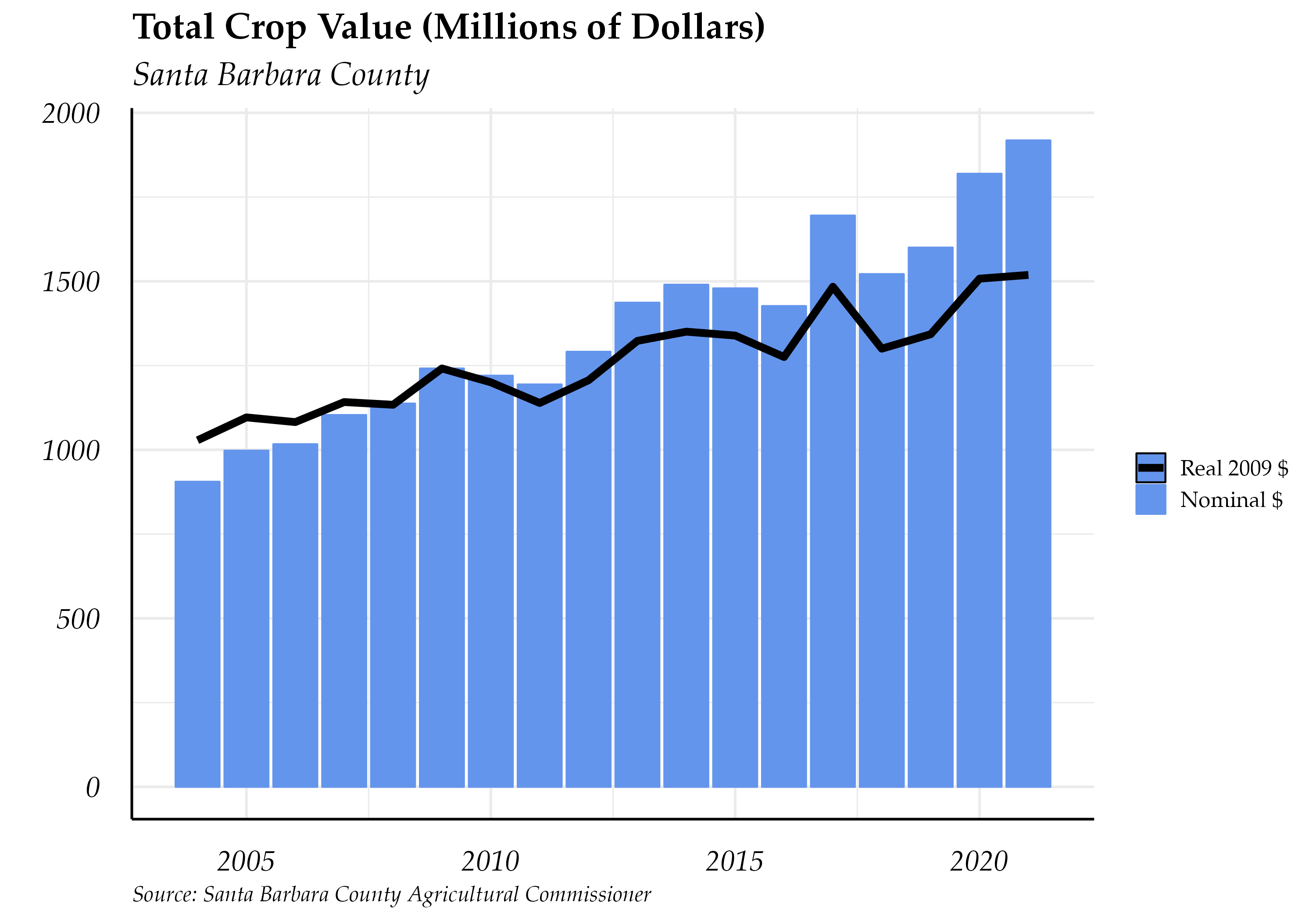

1.3.1 Total Crop Production

The total crop value in 2021 was $1.92, an increase of 5.44% from the prior year. This represents a decline in growth compared with the previous year, when the total crop value increased by 14%. Total harvested acres of vegetables, fruits, nuts and field crops decreased by 0.75%.

1.3.2 Leading Crops

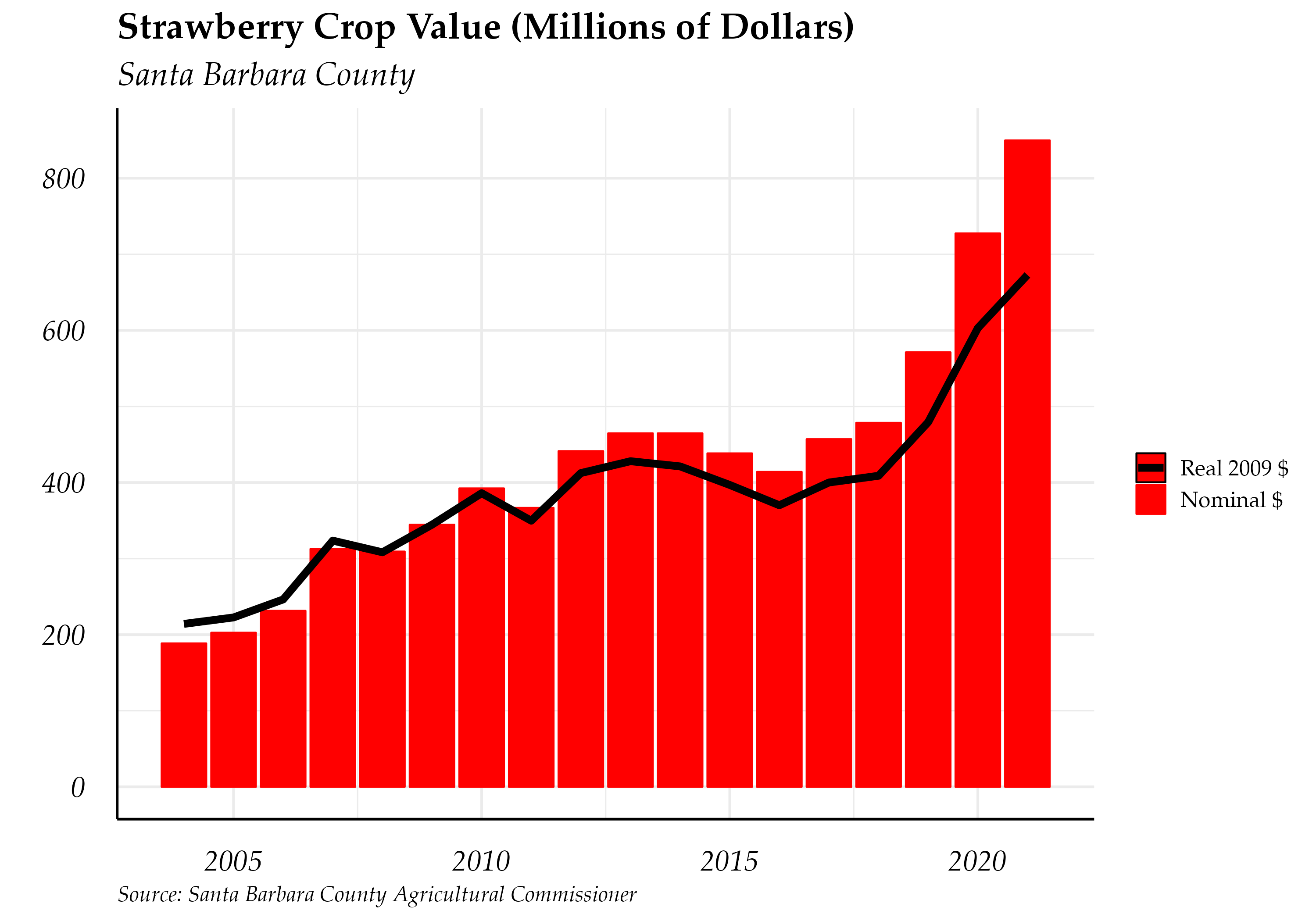

Production of strawberries, the county’s highest-grossing crop for the past 20 years, had a gross value of $849.7 million in 2021. This represents a 16.81% increase in gross value of strawberry crops from 2020, which was $727.4 million. The value of the strawberry crop has nearly doubled in the past decade, and the pace of growth was particularly fast in the past two years. From 2019 to 2020, the strawberry crop’s value grew by 27.35%.

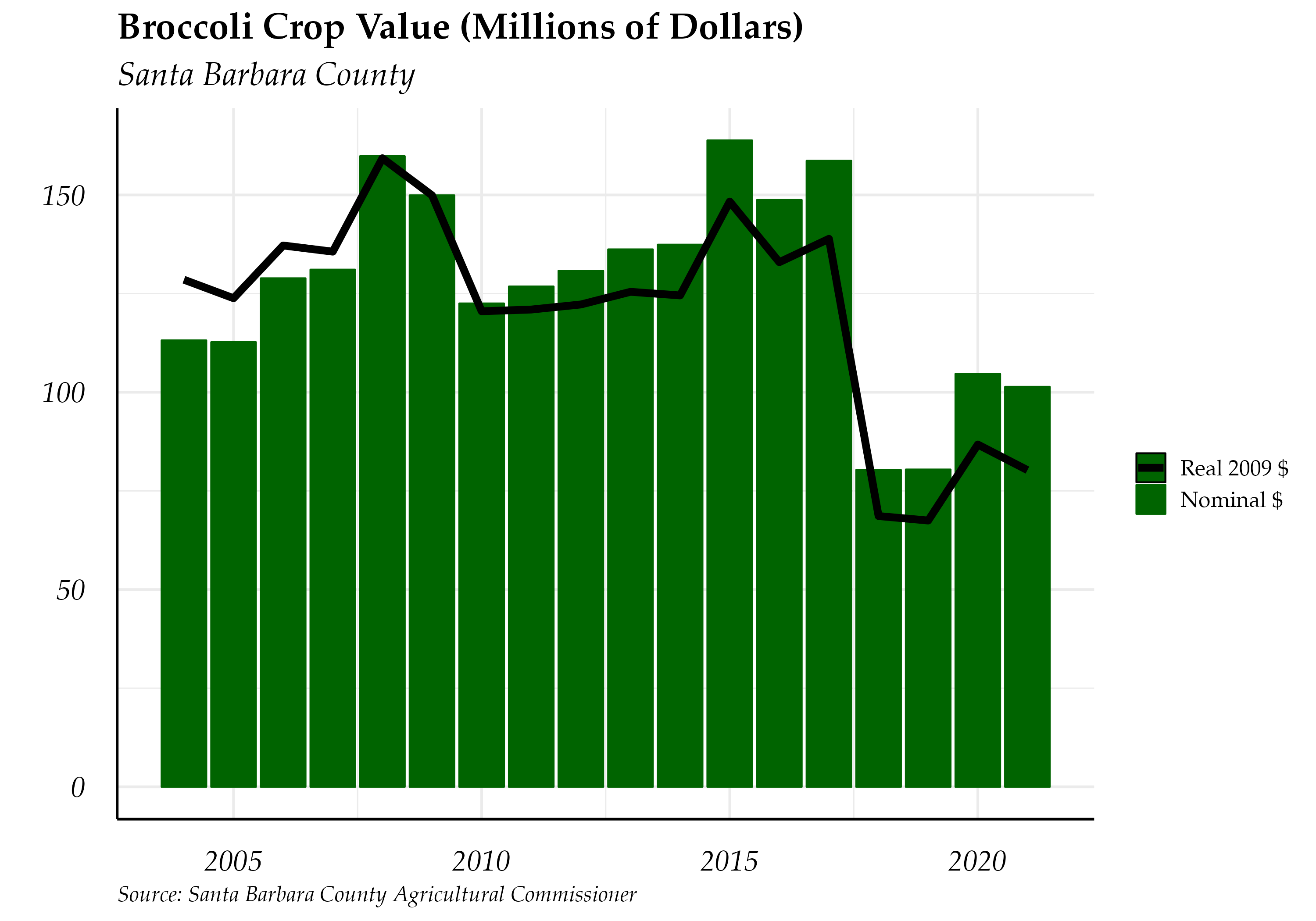

Broccoli’s crop value declined in 2021, decreasing from $104.654 million the previous year to $101.371 million. The 3.14% decrease in gross value reversed the trend from the previous year, when the value of the broccoli crop grew by 30%. Total harvested acres of vegetables, the category that includes broccoli, decreased by -3.79%.

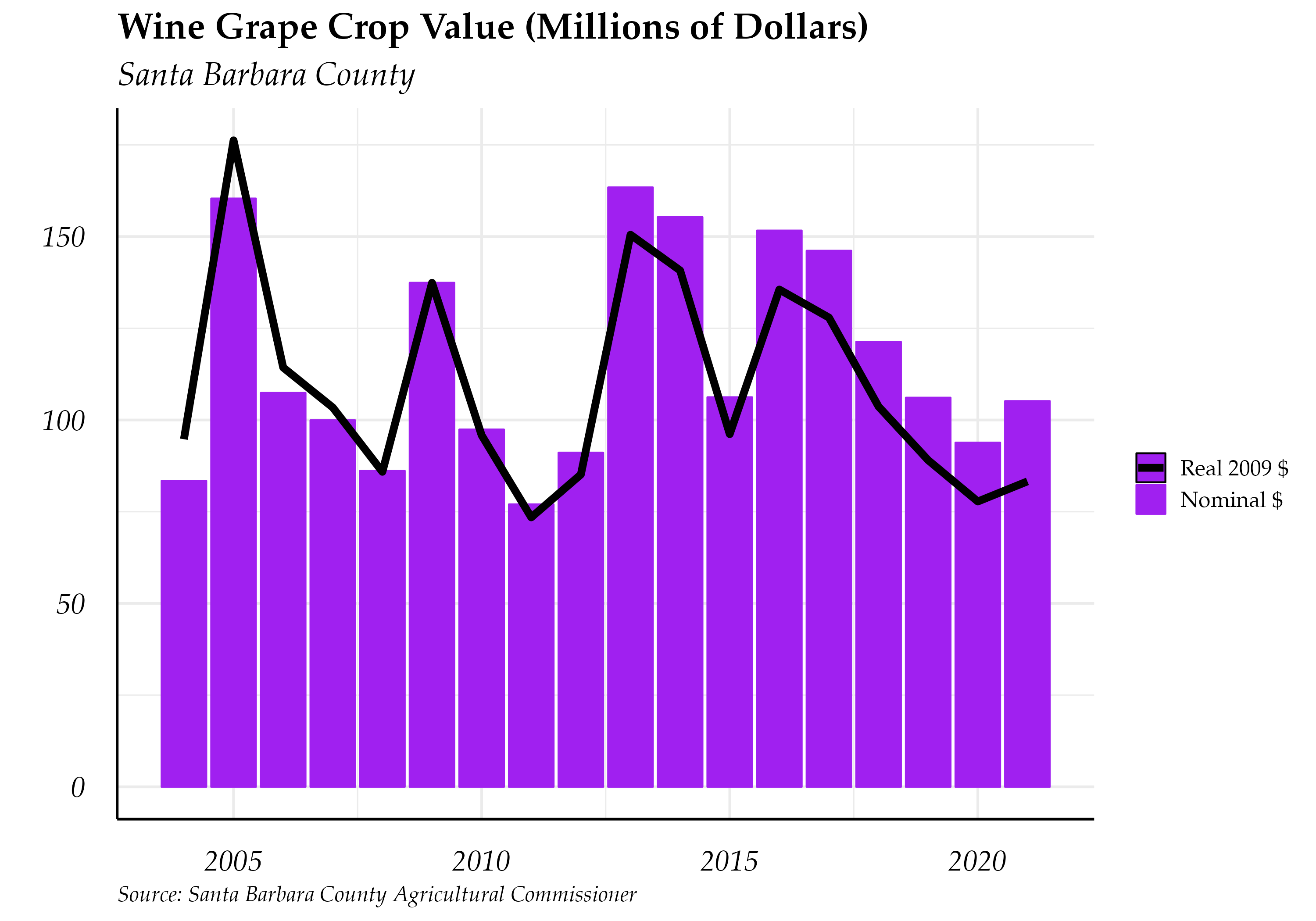

The Santa Barbara County wine grape crop value rose by 12% from $93.84 million in 2020 to $105.15 in 2021. The average price per ton of wine grapes grown in Santa Barbara County increased by 4.12% to $1,958. The average price per ton from 2004 to 2021 was $1,572, well below the price in the past year.

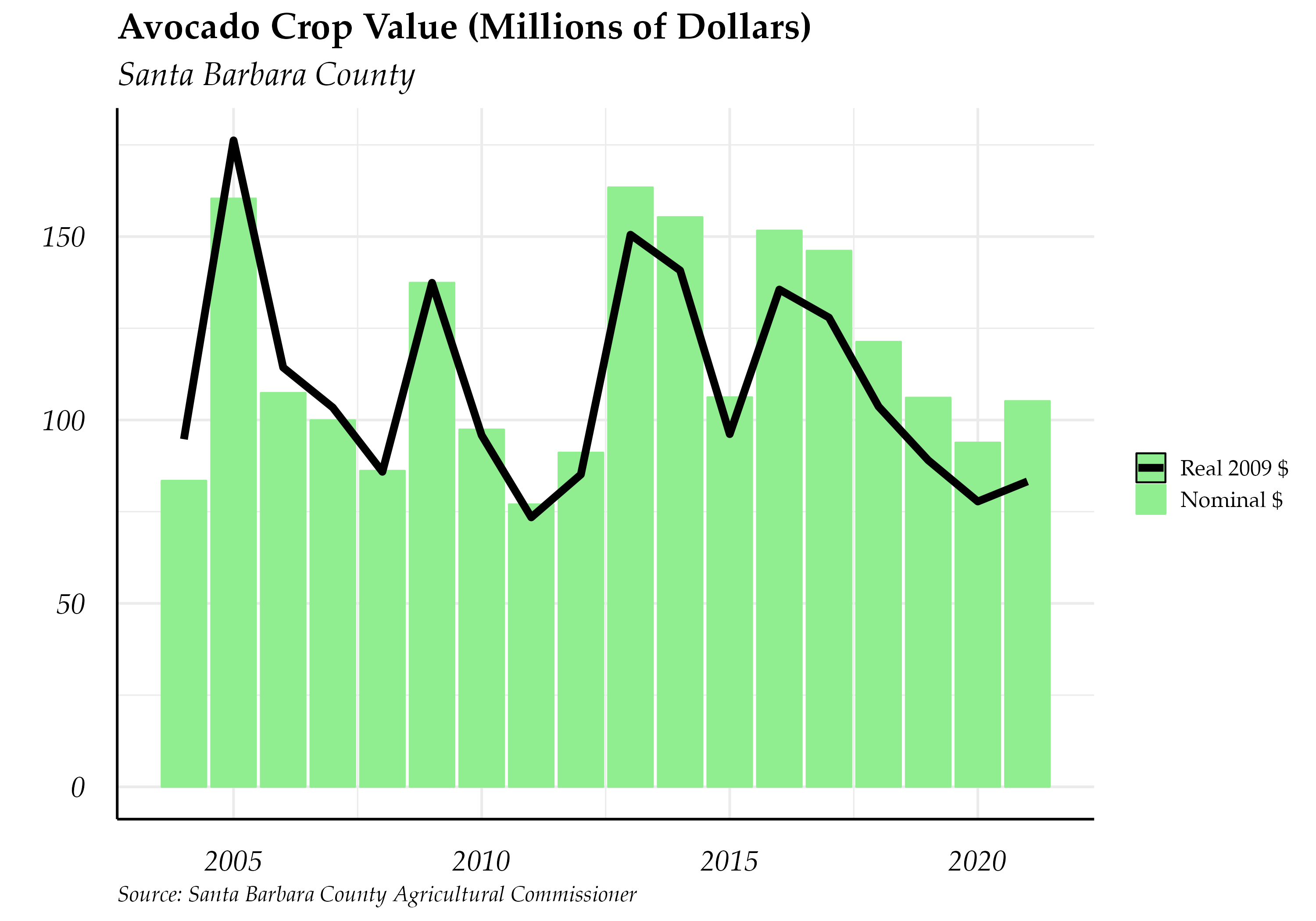

The avocado crop value plummeted by 10% from $80.161 million in 2020 to $50.726 million in 2021. By comparison, the value of the avocado crop increased by 126.37% from 2019 to 2020. The average annual value of the avocado crop from 2004 to 2021 is $47.12 million. In recent years, the avocado crop has experienced more volatility in its value than many other crops.

1.3.3 Wine Grape Production

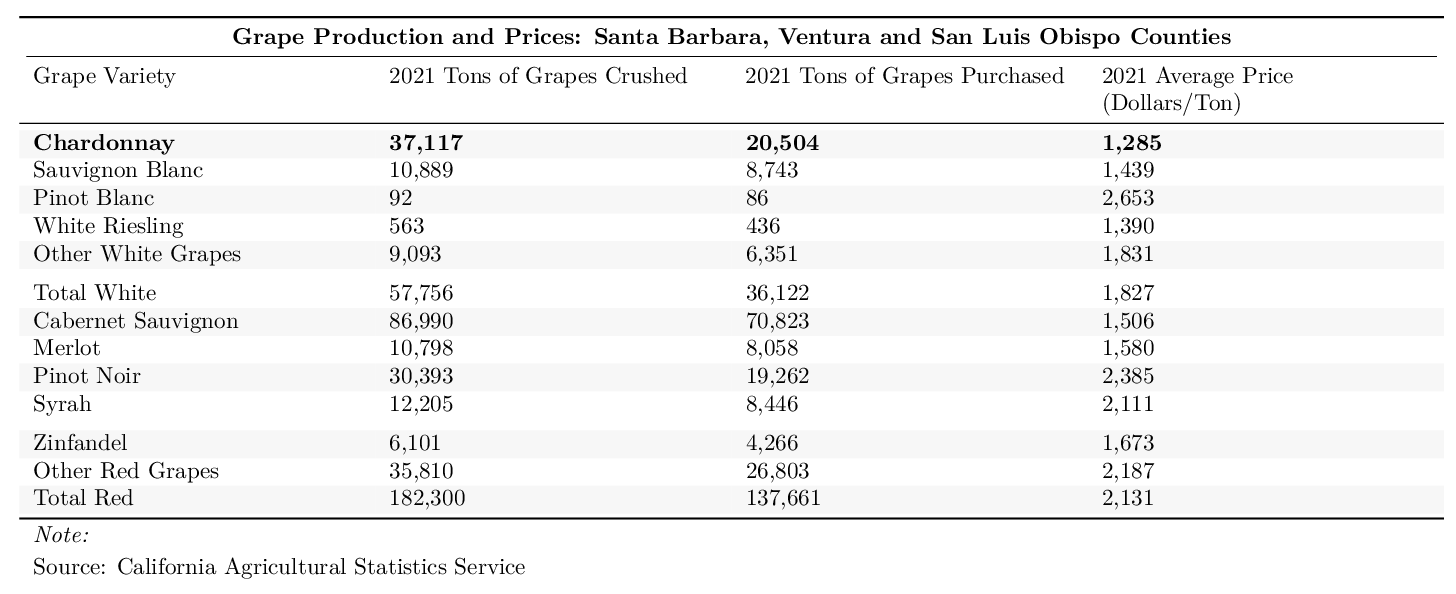

In Santa Barbara, Ventura and San Luis Obispo Counties, the average price of white wine grapes in 2021 was $1827.11 and the average price of red wine grapes was $2131.71. The average price of grapes in the Central Coast region is typically higher than the statewide average. Production of red wine exceeds production of white wine in the tri-county area: in 2021, this region crushed 182300.1 tons of red grapes and only 57756.9 tons of white grapes. Santa Barbara is best known for its Chardonnay and Pinot Noir, the former of which cost $1285.2 per ton and the latter of which cost $2385.02 per ton in 2021. The most heavily produced type of wine in the tri-county area is Cabernet Sauvignon, at 86990.4 tons in 2021.

1.3.4 Drought Recovery

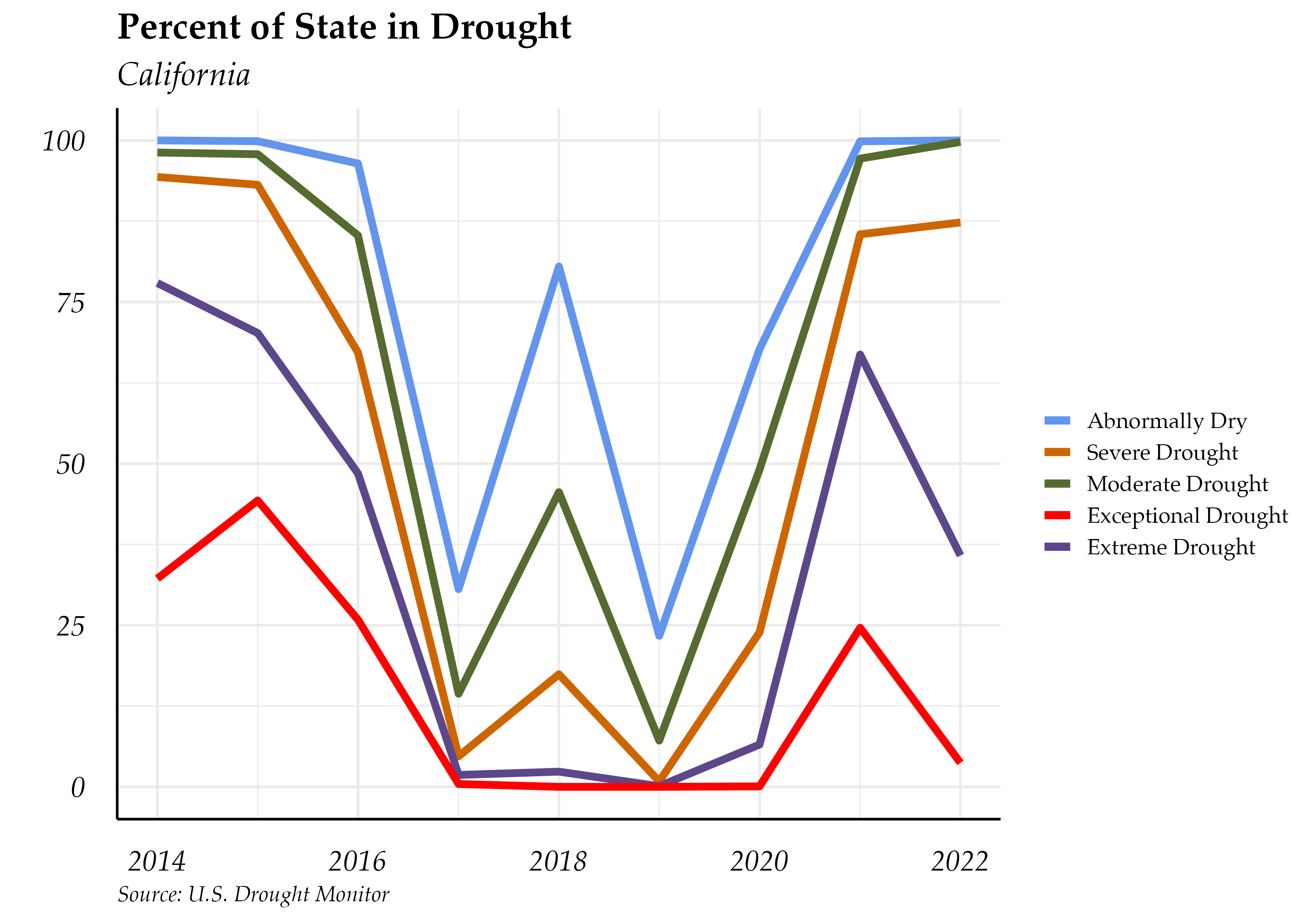

In 2021, 85.47% of California was in a severe drought, a 257% increase from the average in 2020. So far in 2022, the percent of California in a severe or moderate drought has increased by 2.15% and 3%. However, the percent of the state in the most severe drought categories of exceptional drought and extreme drought has declined by -46.48% and -84.92%, respectively.

The percent of Santa Barbara, San Luis Obispo and Ventura counties in the most severe category of exceptional drought has declined substantially since 2014. However, the vast majority of the land in all three counties remains either abnormally dry or in a moderate drought, highlighting the importance of continued water conservation efforts despite improvement in drought status in the last several years.